The Silent Wealth Drain: How Small Payments Keep You Trapped

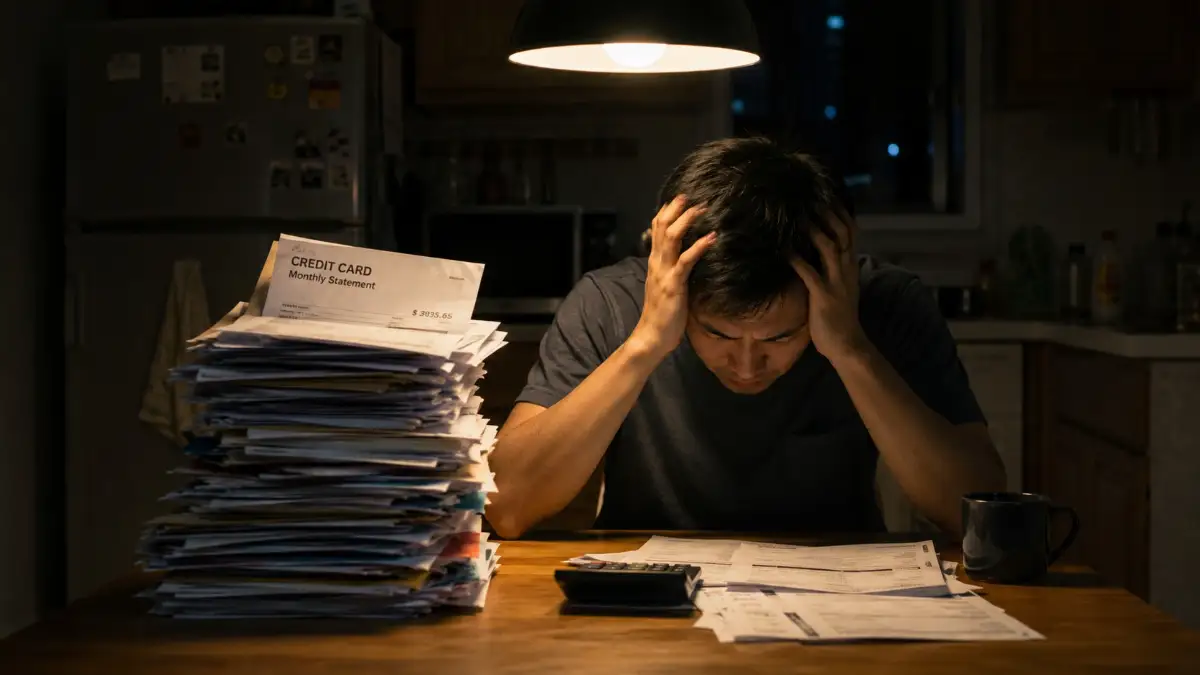

Picture this common scenario in your daily life. You get your monthly credit card statement in the mail or your email inbox. You see a terrifyingly large overall balance at the top of the page. But right below it, there is a much smaller, highly manageable number: the minimum amount due.

You pay that tiny amount, feel a sudden sense of relief, and move on with your busy week. But beneath that temporary comfort lies a massive financial sinkhole. Paying just that fraction feels like you are making real progress. In reality, it is a perfectly designed mathematical trap.

You are blindly feeding a system that slowly eats away at your hard-earned money. You work long, exhausting hours every single week, yet your balance barely moves. Month after month, the numbers stay exactly the same, or even grow larger. It feels like running on a treadmill that keeps speeding up without warning.

You are putting in all the effort, but you are not getting anywhere. So, why do so many smart, hardworking people get stuck in this endless cycle?

The truth is, the financial industry makes things confusing on purpose. Finding honest, clear advice is harder than ever. Because of bad information, average people become long-term victims of the system.

- The Comfort Illusion: Banks always highlight that small payment amount in large, bold letters. They want you to think it is the recommended amount to pay, making you feel completely safe while they quietly charge you massive interest fees in the background.

- Dangerous Advice from Influencers: Many online financial gurus tell you to leverage your debt to get rich quickly. They completely forget to mention that carrying a high-interest credit card balance destroys any potential investment gains you might ever make.

- Complex Fine Print: The actual cost of your daily interest is hidden deep within pages of confusing legal jargon. Most regular people just give up reading and blindly trust the front summary page of their statement.

- The "Good Credit" Myth: Some people mistakenly believe that carrying a small balance from month to month improves their credit score. This is a complete myth that only benefits the rich lenders, keeping you in a constant state of debt.

This endless cycle does not just hurt your bank account. It silently destroys your daily mental well-being and your personal self-esteem.

- Constant Underlying Stress: Even when you are having a fun weekend with your family, the thought of that ever-growing debt lingers in the back of your mind. It silently steals your joy and ruins your mood.

- Shame and Isolation: You might feel too embarrassed to talk about your private financial struggles with your close friends. This forces you to carry a heavy emotional burden completely alone, which leads to depression.

- Fear of the Unknown Future: Every single unexpected expense, like a broken car or a medical bill, becomes a major life crisis. You lose all confidence in your ability to handle basic emergencies because your available credit is already stretched too thin.

- Strained Family Relationships: Money stress is a leading cause of severe arguments at home. The daily tension of never getting ahead creates an invisible distance between you and the people you love the most.

Let us look at a real-life example to make this situation crystal clear. Imagine you buy a brand-new laptop for your side hustle for $1,000.

You put it on a credit card that has a standard 20% annual interest rate. If you choose to only pay a $25 minimum every single month, how long do you think it will take to pay off that single computer? A year? Maybe two years? The shocking reality is that it will take you over five full years to clear that one single purchase.

Worse than the time lost, you will end up paying almost double the original price just in added interest charges. That extra money is cash you could have easily spent on a relaxing family vacation, saved for a rainy day, or invested for your retirement.

When you only pay the lowest amount required by the bank, you are essentially renting your own money at an incredibly high premium.

The credit card companies secretly celebrate when you choose this minimum payment option. They know they have successfully locked you into a highly profitable, long-term contract without you even realizing it.

Every time you swipe that card and pay the minimum, you are funding their massive corporate profits. It is time to wake up and see the harsh reality of this common situation.

You deserve to keep the money you work so incredibly hard to earn every single day. Taking control of this situation requires honesty, courage, and a completely new plan of action.

How to Break Free: Your Step-by-Step Educational Blueprint

Now that we deeply understand the emotional and financial pain of this trap, it is time to take massive action.

You cannot simply wish your credit card balance away. You need a highly structured, logical, and practical plan to defeat the banks at their own game.

I am going to walk you through three clear, actionable steps that you can start applying to your life this very minute.

Face the Ugly Math (Understand the Compound Interest Trap)

The absolute first step to solving any major problem is looking at it clearly under a bright light. Most people avoid logging into their banking apps because the final number causes them physical anxiety.

You must stop hiding from the numbers. To defeat your debt, you need to understand exactly how the math is working against you right now.

Credit cards do not just charge you simple interest once a year. They use a scientific mathematical concept called Daily Compound Interest.

This means that your credit card company calculates your interest charge every single day based on your "Average Daily Balance."

Then, they add that daily interest back into your total principal amount. The very next day, you are literally paying interest on the interest they charged you yesterday.

It is a snowball rolling down a massive hill, picking up speed and size every single second. Let us break down the harsh logic with another real-life scenario.

Suppose you have a $5,000 balance on a card with a 24% Annual Percentage Rate (APR). That 24% is broken down daily.

If your minimum payment is around $150, almost $100 of that payment goes straight into the bank's pocket just for the interest.

Only $50 actually goes toward reducing your $5,000 debt. You are handing over a massive chunk of your income just for the privilege of holding onto their money.

Actionable Advice for Today: Get a simple piece of paper and a pen right now. Log into every single credit card account you own.

Write down three highly specific things for each card: The total balance owed, the exact interest rate (APR), and the current minimum payment due.

Just looking at these numbers written down on a physical piece of paper will give you a massive reality check. It shifts your brain out of the "comfort illusion" and into active problem-solving mode.

You will suddenly realize that paying an extra $20 or $50 a month directly attacks the principal balance, saving you hundreds of dollars in future interest.

Choose Your Attack Strategy (The Snowball vs. The Avalanche)

Now that your numbers are fully exposed, you need a highly specific mathematical strategy to attack them. You cannot just throw random amounts of money at different cards and hope for the best.

In the world of personal finance, there are two scientifically proven methods to destroy debt. These are known as the Debt Snowball and the Debt Avalanche.

Both methods require you to continue making the minimum payments on all your cards, except for one target card. You will throw every single extra dollar you have at that specific target card until it is completely dead.

Let us explore exactly how these two methods work so you can pick the one that fits your personality.

The Debt Snowball Method (Psychology First):

With this approach, you ignore the interest rates completely. You organize your debts from the smallest total balance to the largest total balance.

Your target card is the one with the smallest balance. Why does this work? Human beings are highly emotional creatures.

When you pay off a small $300 balance quickly, your brain releases a massive hit of dopamine. You feel a sudden rush of victory and motivation.

This psychological boost gives you the intense energy needed to attack the next biggest card. It is like losing your first two pounds on a new diet; it proves that the system actually works.

The Debt Avalanche Method (Math First):

With this approach, you completely ignore the total balances. Instead, you organize your cards from the highest interest rate down to the lowest interest rate.

Your target card is the one charging you the highest APR (for example, that terrible 29% store card).

Logically and mathematically, this is the cheapest way to pay off debt. It physically stops the bleeding faster than any other method.

By killing the highest interest rate first, you save the maximum amount of money over the long term. However, it requires a lot of deep patience because it might take months to see that first card hit a zero balance.

Actionable Advice for Today: Look at the paper you created in Step One. If you are someone who gets easily discouraged and needs quick wins, pick the Snowball method today.

If you are a highly logical person who hates wasting a single penny on bank fees, pick the Avalanche method. The specific method you choose matters much less than your commitment to sticking with it.

Automate Your Escape Route to Bypass Human Error

We love to think that we have endless amounts of self-control. We tell ourselves that we will definitely send an extra $100 to the credit card company at the end of the month.

But science tells us a completely different story. Psychologists have proven a concept called Decision Fatigue.

As you go through your busy day making hundreds of small choices at work and home, your brain gets tired. By the time Friday night arrives, your willpower is completely drained.

When you see extra money in your checking account, your tired brain convinces you that you deserve a nice restaurant dinner or a new pair of shoes.

That extra $100 never actually makes it to the credit card company. You fall right back into the minimum payment trap.

The only logical way to beat human error is to completely remove the human from the equation. You must use technology to automate your financial success.

Think of your personal finances like steering a massive cargo ship. If you have to hold the wheel constantly, you will eventually get tired and crash.

But if you turn on the autopilot, the ship steers itself directly to the destination while you sleep. You need to put your debt payoff plan on strict autopilot.

Actionable Advice for Today: Once you have picked your target card from Step Two, go into your main bank account online.

Set up an automatic, recurring transfer that happens the exact same day your paycheck hits your account.

Do not wait until the actual due date of the credit card bill. If you get paid on the 1st of the month, schedule the extra payment for the 2nd of the month.

Force the money out of your hands before you even get a chance to look at it or spend it. If you can only afford an extra $25 above the minimum right now, automate that $25.

You will be deeply shocked at how fast that small, automated extra payment kills the daily compound interest we talked about in Step One.

By forcing the system to work in your favor automatically, you strip the credit card companies of their power. You finally take the control back into your own hands.

You stop being a profitable victim of the system and start becoming the smart architect of your own financial freedom.

Insider Strategies to Accelerate Your Financial Freedom

While setting up automatic payments is a fantastic start, we need to push your progress even faster. Financial experts use specific tools to stop the interest from draining their bank accounts.

You can use these exact same advanced methods to cut your repayment time in half. It just takes a little bit of hidden knowledge and a few smart phone calls.

Let us look at two powerful strategies that banks rarely advertise to their struggling customers. These moves are designed to completely freeze your interest and give you a fighting chance.

The Zero Percent Balance Transfer Hack

If you have a decent credit score, this is one of the smartest moves you can possibly make. A balance transfer simply means moving your existing debt from a high-interest card to a brand-new card.

The trick is finding a new card that offers a 0% introductory interest rate. Many banks offer these promotions to steal customers away from their competitors.

Normally, these zero percent offers last anywhere from 12 to 18 months. Imagine having over a year where every single penny you pay goes directly to your actual balance.

Think of it like carrying a heavy bucket of water that has a massive hole in the bottom. The interest is the water leaking out before you even reach your destination.

A zero percent balance transfer completely plugs that hole. It allows you to finally make real, measurable progress without the bank stealing your efforts.

How to Execute This Properly:

- Check the Transfer Fee: Most banks will charge a one-time fee of 3% to 5% to move your money over. You must calculate if the fee is cheaper than the interest you are currently paying.

- Do Not Add New Debt: Once you move the balance to the new card, you must cut up the old card immediately. If you start spending on the old card again, you will double your financial trouble.

- Set a Strict Deadline: Divide your total balance by the number of zero-percent months you have. Make that exact payment amount every single month so the debt is gone before the standard interest rate returns.

The Secret Phone Call: Negotiating Your Interest Rate

Many people wrongly assume that their interest rate is permanently locked in stone. In reality, credit card companies are highly flexible, especially if you have a history of on-time payments.

Banks spend massive amounts of money trying to acquire new customers. They absolutely hate losing a reliable, paying customer to a rival bank.

You can use this fear to your advantage simply by picking up the phone. All it takes is a polite, clear conversation with a customer service representative.

A Simple Script You Can Use Today:

Call the number on the back of your card and politely ask to speak with the retention department. Say something like, "I have been a loyal customer for a long time, but my current interest rate is too high."

Next, mention that you have been looking at a competitor's card offering a much lower rate. Then ask, "Can you lower my current APR so I can keep my account with you?"

Sometimes they will say no, and that is completely fine. But very often, they will instantly drop your rate by a few percentage points just to keep you happy.

Even a tiny drop from 24% to 19% can save you hundreds of dollars over the course of a year. It is literally free money for a ten-minute phone call.

Building a Long-Term Maintenance System

Getting out of the minimum payment trap is an incredible achievement. However, staying out of that trap for the rest of your life is the ultimate goal.

You need a personal financial system that protects you from falling backward into old habits. Your future peace of mind depends on changing how you view credit entirely.

The golden rule of credit card use is incredibly simple but highly effective. You must treat your credit card exactly like a debit card.

Never swipe your plastic unless you already have the physical cash sitting in your checking account to back it up. If you cannot afford to pay for that new television in cash today, you cannot afford to put it on credit.

To maintain your new financial health, change your automatic bank settings immediately. Instead of setting your auto-pay to the "Minimum Amount Due," switch it to "Full Statement Balance."

This one tiny settings change guarantees you will never pay another penny in credit card interest again. You will get to enjoy all the security and fraud protection of a credit card without paying the hidden taxes.

Dangerous Roadblocks: 5 Major Traps to Avoid

As you begin this journey toward financial stability, you will face several common temptations. The road to being debt-free is rarely perfectly smooth.

Many well-meaning people accidentally sabotage their own progress because they do not understand the system. Let us walk through the biggest mistakes you must avoid at all costs.

1. Chasing Reward Points While in Debt

Credit card companies aggressively market their travel miles, cash back, and shiny reward points. They make you feel like you are missing out on free money if you do not use their card for every single purchase.

Here is the harsh reality of the situation. If you are carrying a balance and paying 20% in interest, getting 2% cash back is completely meaningless.

You are losing massive amounts of money just to earn a tiny fraction back in points. The math simply does not work in your favor.

The Consequence: You will keep spending money you do not have just to hit reward targets. Freeze your card usage entirely until your balance reads absolute zero.

2. Closing Your Account the Moment It Hits Zero

When you finally pay off that stressful credit card, your first instinct will be to call the bank and close the account forever. It feels like the ultimate form of revenge against the lender.

However, closing an old account can actually damage your credit score significantly. A big part of your credit score is based on your "Credit Utilization Ratio."

This ratio compares how much debt you currently owe against your total available credit limit. When you close a card, you instantly wipe out a huge chunk of your available credit limit.

The Consequence: Your credit score might suddenly drop, making it much harder to buy a house or finance a car later on. Instead of closing the account, just cut up the physical card and keep the account open with a zero balance.

3. Draining Your Emergency Savings Completely

Sometimes people get so intensely motivated to destroy their debt that they throw every single penny they own at the credit card. They empty their entire savings account just to see that credit card balance drop faster.

This is a highly dangerous strategy because life is completely unpredictable. Cars break down, roofs leak, and medical emergencies happen when you least expect them.

If you have zero cash in the bank when a crisis hits, what will you do? You will be forced to reach right back for that credit card.

The Consequence: You will end up right back in the exact same debt trap, but this time you will feel utterly defeated and depressed. Always keep a basic emergency fund of cash in the bank, even while paying off your high-interest debt.

4. Viewing Credit as an Extension of Your Income

Many hardworking individuals make the mistake of looking at their credit limit as extra spending money. They view a $10,000 credit limit as $10,000 of wealth they somehow own.

This mindset is exactly what banks pray you will adopt. That credit limit is not your money; it is a highly expensive loan waiting to happen.

The Consequence: You will constantly live beyond your actual means, spending future paychecks before you even earn them. You must mentally separate your actual bank balance from your available credit limits.

5. Falling for "Quick Fix" Debt Settlement Scams

When people feel completely overwhelmed by massive monthly payments, they often look for an easy way out. You might see late-night advertisements for companies promising to magically erase your debt for pennies on the dollar.

These debt settlement programs often tell you to stop paying your credit cards completely. They claim they will negotiate a secret deal with your bank on your behalf.

The Consequence: These shady companies often charge massive hidden fees while completely destroying your credit score in the process. Your bank might even sue you for the unpaid balance before any settlement is reached. Always manage your own payments or speak directly to a certified non-profit credit counselor instead.

Your New Path Forward Starts Right Now

You now have a crystal-clear understanding of exactly how the minimum payment trap operates behind the scenes. More importantly, you possess the exact tools required to dismantle it permanently.

You no longer have to live with that heavy feeling of dread sitting in your chest every single time the mail arrives. You have the power to stop the endless cycle of throwing your hard-earned money away on invisible interest charges.

Taking control of your personal finances is one of the most empowering things you will ever do in your life. It is not just about the math; it is about reclaiming your personal freedom.

When you eliminate this heavy burden, a whole new world of opportunities opens up for you. You can finally start saving for that dream vacation, building a secure retirement, or simply sleeping deeply through the night without worry.

Remember, the absolute hardest part of this entire journey is simply starting. Do not wait for a magical perfect moment or a sudden raise at work to begin fixing this issue.

Grab that piece of paper, log into your accounts, and look at your numbers honestly today. Set up that very first automated extra payment, even if it is just a tiny amount.

Every single extra dollar you send is a direct blow to the bank's system and a massive win for your family's future. You are smart enough to break this cycle, and you absolutely have what it takes to win.

Stay deeply focused on your end goal, trust the mathematical process we discussed, and watch your financial stress slowly melt away. Your future self is going to be incredibly grateful for the brave choices you are making right now.